The death warrant for unfettered globalisation has been executed, paving the way for a stark new era of economic polarisation a “highway or my way” theory of trade and influence. While European powers have long practised a subtler form of economic self-interest, the US is now openly championing this fractured approach.

From the aggressive “America First” tariffs on steel and aluminium under the previous administration to the current administration’s CHIPS and Science Act, openly incentivising domestic semiconductor manufacturing and effectively shunning foreign production, the message is clear: nations are increasingly drawing lines in the economic sand, prioritising national interests and creating distinct, often competing, spheres of influence. This overt shift signals a profound reordering of global commerce, where alliances are transactional and economic advantage is pursued with unprecedented assertiveness.

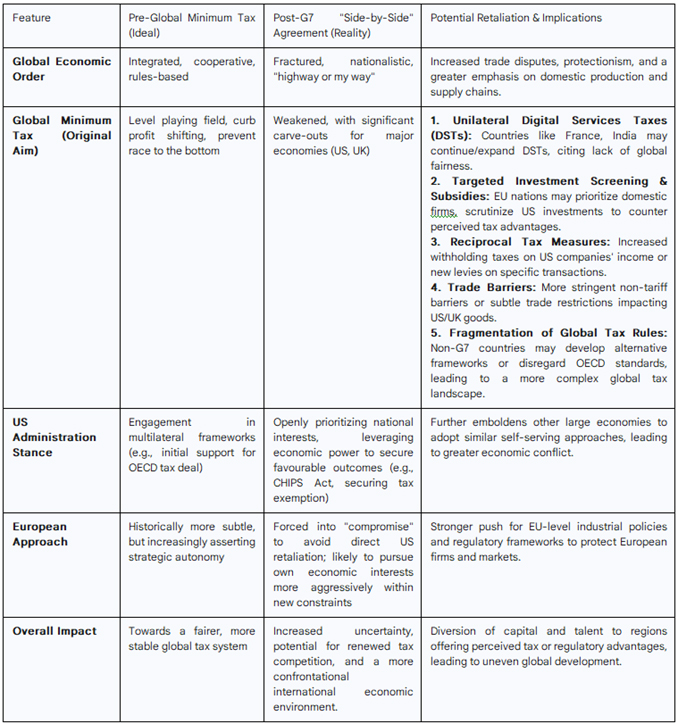

Adding a fresh layer to this unfolding drama, the recent G7 agreement to endorse a “side-by-side” system for the global minimum tax has sent ripples through the international tax landscape. Under this new agreement, US & UK-parented multinational corporations would effectively be shielded from certain key provisions of the Organisation for Economic Co-operation and Development (OECD’s) Pillar Two rules, particularly the Income Inclusion Rule (IIR) and Undertaxed Profits Rule (UTPR). This move, reportedly a concession to the US after it threatened revenge taxes on countries applying the global minimum tax to US firms, allows American and British companies to be primarily taxed domestically, even if their effective global tax rate falls below the 15% minimum.

The Retreat from Unilateralism and the Price of “Compromise”

The G7’s decision, while framed as a way to “stabilise and provide certainty” to the international tax system, is widely seen by critics as a carve-out that could significantly undermine the global minimum tax initiative. The original intent was to create a level playing field, curb profit shifting, and prevent a “race to the bottom” in corporate taxation. This new “side-by-side” approach, however, grants US and UK firms a degree of protection that companies from other nations may not enjoy.

This situation directly reflects the “highway or my way” theory in action. The US, backed by the threat of retaliatory measures, such as the now-withdrawn Section 899 of a proposed US tax bill, has secured an outcome that heavily favours its domestic interests. While some European officials might see this as an “honourable compromise” to avert a broader tax war and protect their own companies from US retaliation, it sets a precedent that could encourage other large economies to demand similar exemptions.

The Looming Spectre of Retaliation and Economic Fragmentation

The most significant implication of this G7 agreement is the potential for retaliation by European and other developed countries, and even developing nations, who have invested significant political capital and legislative effort into implementing the global minimum tax. Here is how such retaliation might manifest, with examples:

In essence, the G7’s recent tax agreement, rather than cementing a truly global and equitable minimum tax, risks deepening the trenches of economic nationalism. By openly accommodating the interests of one or two powerful nations, it validates a transactional approach to international economic cooperation, almost daring other major players to respond in kind. The result is likely to be not a unified global economy, but a more complex and confrontational landscape of competing economic blocs, each vying for advantage.

The G7’s recent move regarding the global minimum tax is a stark illustration of this new, polarised economic reality. Far from cultivating a truly level playing field, it underscores that major powers are now openly carving out exceptions to suit their national interests, often under the implicit threat of retaliation.

This “side-by-side” system, while perhaps averting an immediate tax war, effectively signals a retreat from genuine multilateralism and invites other nations to pursue similar exemptions. The consequence is not a more stable global economic system, but a more fragmented one, where economic “peace” is purchased at the price of equity, and the pursuit of national advantage increasingly outweighs the collective good.

The world is unequivocally moving towards an era of economic blocs and bilateral deals, where the high road of shared prosperity is increasingly abandoned for the self-serving path of “my way”.